Florida Medicaid expansion alternative shows a different path for Ohio

Jul 23, 2013

Obamacare was billed as a comprehensive healthcare solution for the poor and the uninsured—a goal that it sought to accomplish largely by forcing states to expand Medicaid coverage to these groups. However, as the Buckeye Institute has argued for months, now that the Supreme Court has made Medicaid expansion optional for the states, there are alternatives to going all-in on Medicaid’s busted flush: states can develop market-based solutions around their citizens’ unique needs. As an example, Florida’s House of Representatives recently passed such a plan. Although the State Senate ultimately did not approve it, the potential remains for Florida (or any other state) to develop a specialized Medicaid alternative that provides better coverage at a lower cost.

Florida’s plan was designed to help those who would otherwise be in the “expansion population” purchase private insurance. Parents and disabled adults in the gap between the cutoff point for Medicaid in Florida (22%/74% of the Federal Poverty Line, respectively) and the level at which they are eligible for subsidies in the federal exchange would be given $2,000 annually, which would be paid into a health savings account (HSA). $2,000 is enough to cover all healthcare spending by 82% of covered persons, who typically demand fewer healthcare services. The HSA, along with personal contributions, would be used to purchase private insurance through a state-run clearinghouse. Low-income people with private insurance have better access to medical care relative to those on Medicaid—despite consuming less in healthcare than it costs Medicaid to cover them. In this way, Florida’s plan had notable advantages compared to accepting the expansion wholesale.

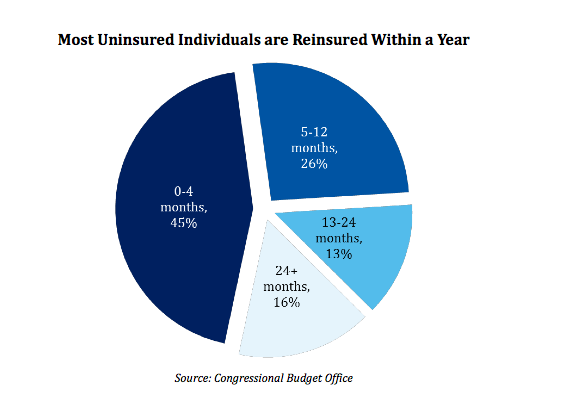

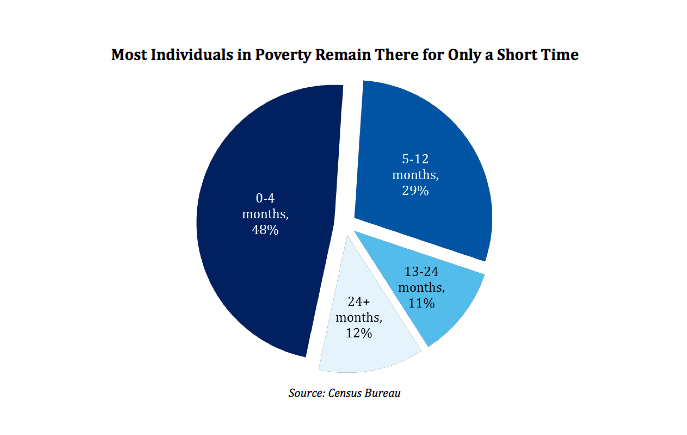

Florida’s HSA plan had several distinct advantages over the federal exchange as well. Unlike the Obamacare exchanges, Florida’s clearinghouse would have allowed a considerable amount of variety in the plans offered. This gets to the key advantage of Florida’s plan, and to Medicaid alternatives in general: allowing consumers to self-select the features they need. Given that 71% of uninsured people in Florida only remain so for twelve months or less, and that 87% of people below the poverty line only remain so for two years or less, the option of less expensive short-term policies will better suit most of those receiving aid. This type of flexibility is not possible under the rigid framework of the federal exchange, which sets strict requirements for the plans offered.

The Medicaid expansion, by its terms, operates as a uniform entitlement and is almost impossible to modify in a meaningful and permanent way to meet the unique needs of the sundry states and populations it serves. Conversely, a state-run plan can incorporate all of the reforms the particular state needs, and self-corrects to meet the needs of the citizens. These traits translate into lower costs: the sponsors of the Florida plan estimated it would cost the state less than a quarter of what expanding Medicaid would. State legislatures who are cognizant of their state’s needs could, using Florida’s plan as a template, develop a way to meet these needs in a more cost-effective way than what the federal government is offering. The Florida House’s creativity should be looked to by Ohio policymakers as they grapple with deciding how best to care for the poor and uninsured in a way that does not put Washington D.C. in the driver seat.